")

TL;DR: Ahead of Budget 2026, India’s digital asset industry — represented by groups like the Bharat Web3 Association and major exchanges — is asking the Finance Ministry for two specific changes. First, they want to reduce TDS on digital asset transactions from 1% to 0.01%. Second, they ask to allow investors to offset losses against gains, similar to how equity taxation works. Neither change has been confirmed. Whatever happens, structured real estate platforms operate under separate legal frameworks (typically a Trust or SPV). They do not depend on crypto-specific tax policy to function.

Budget 2026 Crypto Tax: What’s Actually Being Proposed, and Why It Matters Beyond Crypto

India’s current tax treatment of digital assets includes a 1% Tax Deducted at Source (TDS) on every sell transaction. As Budget 2026 discussions heat up, industry groups are pushing for changes to that framework. Here’s what’s actually being asked for. Here’s what it would mean if adopted, and why this conversation matters even for people who aren’t trading crypto directly.

What is the industry actually asking the Finance Ministry for?

Two specific, concrete proposals are driving the Budget 2026 crypto tax conversation, according to industry groups including the Bharat Web3 Association and major Indian exchanges:

Reduce TDS from 1% to 0.01%. The current 1% TDS on every sale gets deducted regardless of whether the trade was profitable. This ties up capital and discourages frequent trading activity. The industry argues a much lower rate would still let the government track transactions — its stated purpose. It would do so without pulling as much liquidity out of the market.

Allow loss set-off against gains. Under current rules, if you lose money on one digital asset transaction and profit on another, you’re taxed on the gain without being able to offset it against the loss. This is unlike equity markets, where net gains (after offsetting losses) are what gets taxed. The industry is asking for the same treatment to apply here.

Neither proposal has been confirmed or rejected as of this writing — these are industry asks heading into budget discussions, not announced policy.

Why would this matter for real estate investors, not just crypto traders?

It’s a fair question if you’re investing in tokenized land rather than trading cryptocurrency directly. The connection is that Real World Assets (RWAs) — including tokenized real estate — typically rely on blockchain infrastructure. Tax policy affecting digital asset transactions broadly can affect how liquid and active that infrastructure’s secondary markets become. A high transaction tax creates friction for anyone trying to transfer a digital ownership unit, regardless of whether the underlying asset is a cryptocurrency or a fractional interest in land.

That said, it’s worth being precise about the connection: tax policy on crypto trading and the legal structure underlying real estate tokenization are related but distinct things. Lower transaction taxes could make secondary transfers smoother. However, they wouldn’t change the underlying legal protections of a specific real estate investment.

Does this affect how platforms like Landbitt are structured?

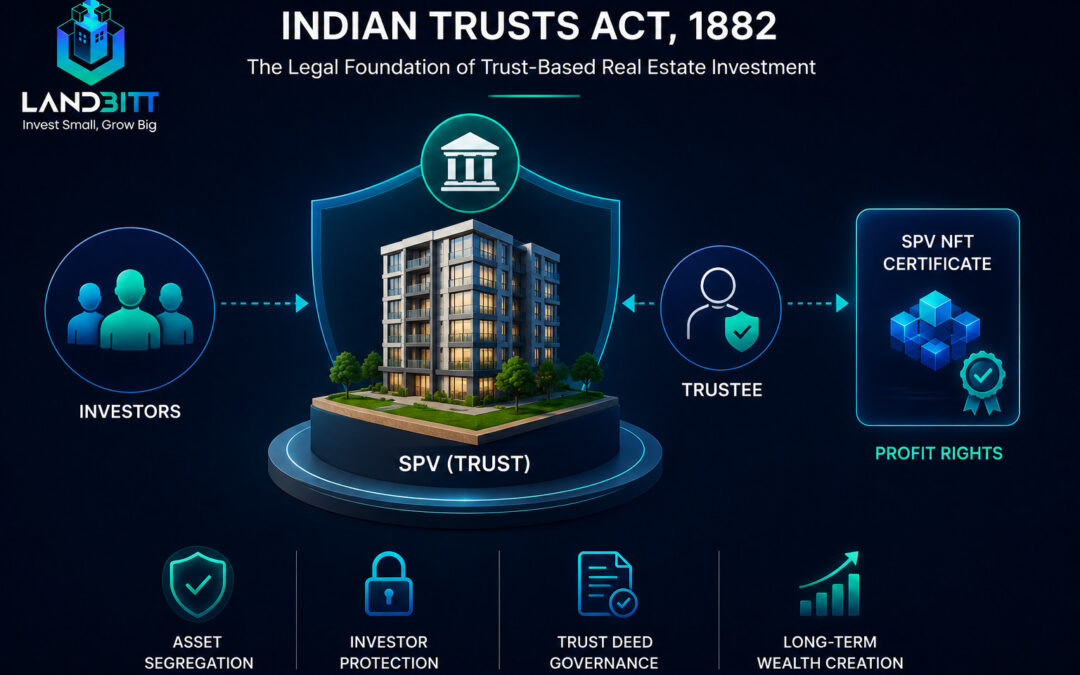

No — and that’s worth being clear about regardless of how the budget discussion resolves. Structured real estate platforms typically hold the underlying property through a Trust or SPV (Special Purpose Vehicle), with investors holding a beneficial interest in that structure. This legal framework operates independently of crypto-specific tax policy. It’s a separate legal apparatus, governed by trust and property law, not by how digital asset trading gets taxed.

Ownership records may be tracked on a blockchain network for transparency, but that’s a recordkeeping layer — it doesn’t change the underlying legal protections. It doesn’t depend on the Budget 2026 outcome to keep functioning. For the actual mechanics of that structure, see our guide on real estate tokenization in India.

How might emerging fintech hubs factor into this?

Cities developing fintech and financial services infrastructure — Ahmedabad’s GIFT City is a frequently cited example — are often mentioned in discussions about how clearer digital asset tax policy could attract institutional capital. Whether that materializes depends on the specific policy outcome and a range of other factors. It’s a plausible direction rather than a settled prediction.

What should investors actually take from this, regardless of outcome?

Budget proposals are exactly that — proposals, until they’re actually enacted. Whatever happens with crypto-specific tax policy, the legal soundness of a specific real estate investment depends on its own structure (proper Trust or SPV documentation, KYC compliance, transparent reporting). It does not depend on broader digital asset tax reform. Evaluate any specific investment on those fundamentals rather than on anticipated policy changes that haven’t happened yet.

Related guides

Frequently Asked Questions

What is the industry asking for in Budget 2026 regarding crypto tax?

Two main changes: reducing TDS on digital asset transactions from 1% to 0.01%, and allowing investors to offset losses against gains, similar to equity taxation.

Has the government confirmed these changes?

No. As of this writing, these are industry proposals ahead of budget discussions, not confirmed policy.

Does crypto tax policy affect real estate tokenization platforms directly?

Indirectly, through shared blockchain infrastructure and secondary-market liquidity — but the underlying legal structure (a Trust or SPV holding the property) operates independently of crypto-specific tax rules.

Is my investment in a tokenized property dependent on this budget outcome?

No. The legal protections behind a properly structured Trust or SPV investment don’t depend on how digital asset trading gets taxed — that’s a separate legal framework.

Why do TDS rates matter for digital asset liquidity?

A high transaction tax on every sale discourages frequent trading and ties up capital, which can reduce how liquid a secondary market becomes — a lower rate is generally argued to support more active markets while still letting transactions be tracked.