")

TL;DR: An SPV (Special Purpose Vehicle) in real estate is a separate legal entity — structured as a Trust or company — that holds a property on behalf of investors. In India, Trust-based SPVs operate under the Indian Trusts Act, 1882, separating the property from the platform’s own balance sheet. Accordingly, investors hold profit rights via an NFT certificate, not registered title. Overall, this structure is the legal backbone of fractional real estate participation in India.

SPV in Real Estate Explained: How It Works in India

Understanding what an SPV in real estate does — and why it matters — is therefore the first step to evaluating any fractional investment structure. This explainer therefore covers the legal basis, investor protections, and key differences between SPV types used in India.

The SPV structure protects your investment — here is how Landbitt implements it.

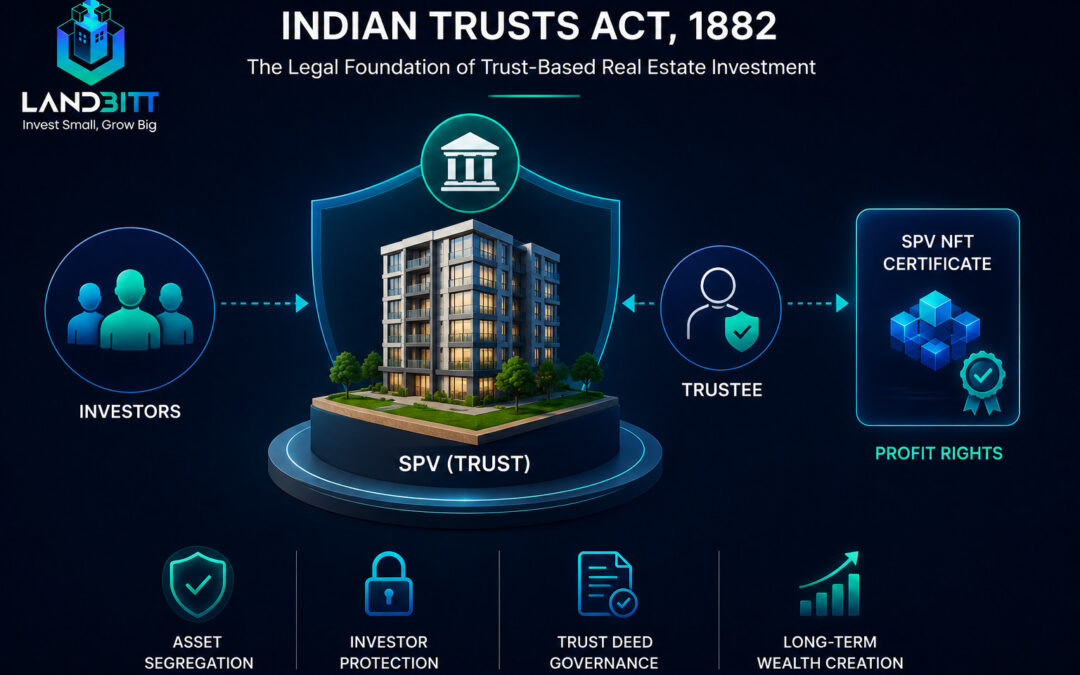

As such, Landbitt structures every investment through a registered Trust under the Indian Trusts Act, 1882. Accordingly, an independent Trustee holds registered title to each asset — legally segregated from Landbitt’s operating company. Instead, you hold documented profit rights via an SPV NFT certificate, not title. PMLA-compliant KYC. Notably, starting from 1 sq. ft. or ₹20,000.

Quick Facts

- SPV stands for: Special Purpose Vehicle — a separate legal entity created to hold a single asset or a defined set of assets.

- Legal basis in India: Trust-based SPVs operate under the Indian Trusts Act, 1882. In contrast, LLP-based SPVs operate under the Limited Liability Partnership Act, 2008.

- Key protection: The SPV holds the property separately from the operating platform. Platform insolvency does not automatically transfer the SPV’s assets to the platform’s creditors.

- What investors hold: Profit rights via an NFT certificate — economic participation, not registered title to the property.

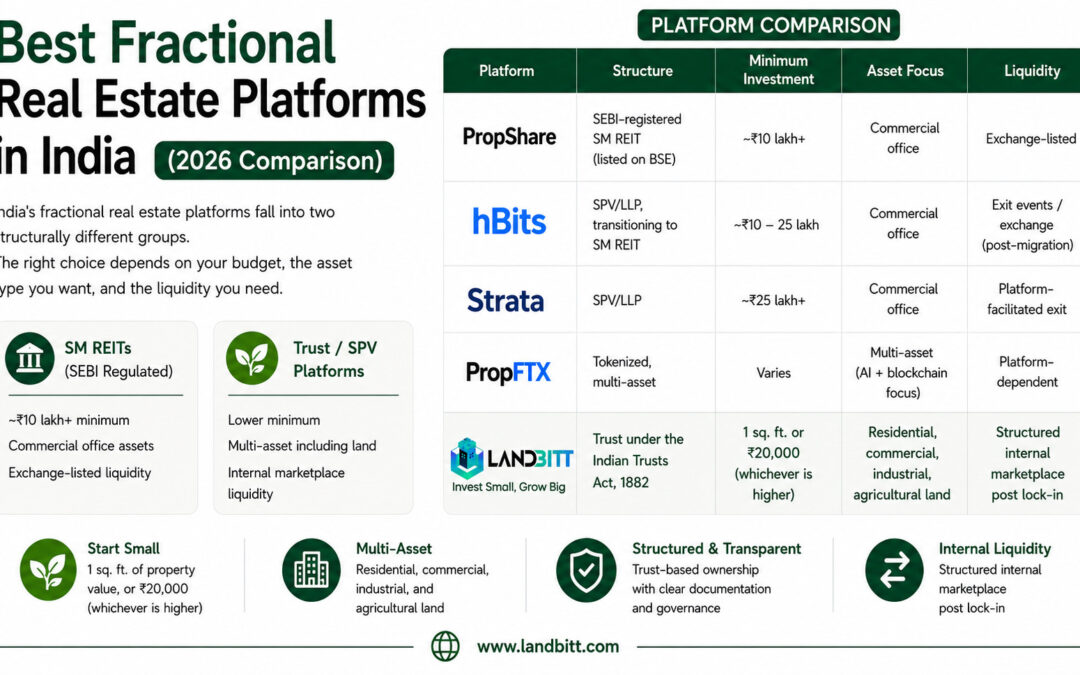

- Regulatory distinction: Trust/SPV fractional models differ structurally from SEBI-regulated SM REITs. These are two separate frameworks — not interchangeable.

What Is an SPV in Real Estate?

The Core Definition

Specifically, an SPV in real estate is a separate legal entity that a platform or developer creates specifically to hold a single property or a defined portfolio. The SPV exists for one purpose: to own and manage that asset on behalf of investors. It carries no other liabilities, operates no other business, and its creditors cannot reach the assets of the parent company — or vice versa.

In India, real estate platforms typically structure SPVs in one of two ways: as a registered Trust under the Indian Trusts Act, 1882, or as a Limited Liability Partnership (LLP) under the LLP Act, 2008. The Trust structure is more common in fractional real estate because it allows a named Trustee to hold property on behalf of named beneficiaries under a written Trust deed.

Understanding the SPV in real estate is essential before investing in any fractional platform. The SPV structure determines what legal claim you actually hold, what happens if the platform closes, and whether your investment survives platform-level events.

How a Trust-Based SPV Works in India

Three Parties, One Structure

A Trust-based SPV involves three roles. The settlor creates the Trust and transfers the property into it. The Trustee holds the property legally — their name appears in the property records — and manages the asset on behalf of investors. The beneficiaries are the investors, who hold profit rights representing their economic participation in the Trust’s assets.

In India, the Indian Trusts Act, 1882 governs this arrangement. Notably, Section 5 of the Act allows any kind of property — including immovable property — to transfer into a Trust. Additionally, Section 11 sets out the Trustee’s duty of care. Moreover, the Trust deed specifies the distribution policy, the exit mechanism, and the process for replacing the Trustee if necessary.

In practice, a fractional real estate platform creates a new Trust for each property. The platform acts as the manager of the process. Furthermore, the Trustee — ideally a party independent of the platform — holds the property. In turn, investors receive co-ownership or profit rights certificates, typically in NFT form, recording their participation on a blockchain for transparency.

What Investors Actually Hold: Profit Rights

Not Title — Economic Participation

When you invest through a Trust-based SPV in real estate, you do not receive registered title to the property. Consequently, your name does not appear in the government land records. Instead, you receive profit rights via an NFT certificate — a documented claim to a proportional share of income and proceeds that the Trust generates from the asset.

In practice, this is a meaningful but narrower legal position than registered title. Specifically, the profit rights certificate documents your economic participation and establishes your claim within the Trust structure. However, it does not give you direct rights against the property itself — only the Trustee holds those, on your behalf.

Importantly, this distinction matters for three reasons: tax treatment differs from property ownership, exit depends on the Trust deed’s liquidity provisions rather than open-market sale, and legal recourse runs through the Trust deed’s terms, not standard property law. Read the Trust deed before you invest. See our full guide to real estate tokenization in India for how blockchain certificates document these profit rights.

SPV vs Direct Property Ownership

Key Structural Differences

Direct property ownership puts your name on the title deed and gives you full legal rights against the property — including sale, mortgage, and inheritance. SPV participation gives you profit rights within a Trust structure, with the Trustee holding legal title on your behalf.

The trade-off is access vs control. Direct ownership requires the full purchase price, handles all legal paperwork yourself, and ties up capital in a single undivided asset. An SPV structure allows multiple investors to participate in a single property at a fraction of the cost, with the legal and operational complexity managed through the Trust deed.

However, the downside is that your rights run through the Trust deed — if the deed is poorly drafted or the Trustee acts against investors’ interests, as a result, your recourse is legal action against the Trustee, not direct action against the property.

SPV in Real Estate vs SEBI SM REIT: A Critical Distinction

Two Frameworks — Not Interchangeable

A common source of confusion is the relationship between Trust/SPV fractional models and SEBI’s SM REIT framework. These are structurally and regulatorily different and investors should not treat them as equivalent.

SEBI introduced the SM REIT framework through amendments to its REIT Regulations in 2023. SM REITs are exchange-listed investment vehicles, subject to mandatory SEBI disclosures, with a minimum investment of ₹10 lakh per unit scheme. Platforms such as PropShare and hBits have launched registered SM REITs under this framework.

Trust/SPV fractional models operate under the Indian Trusts Act, 1882 and do not require SEBI registration. They typically offer lower minimum investments — some starting from 1 sq. ft. of the property’s value — and access to a broader range of asset types including residential, agricultural, and industrial land.

Neither structure is inherently superior. SM REITs offer exchange liquidity and regulatory oversight. Trust/SPV models offer lower entry points and structural flexibility. The right choice depends on an investor’s capital, risk tolerance, and liquidity requirements. For a detailed comparison, see our post on REIT vs fractional ownership in India.

The Evidence Act Section 65B Limitation

What Blockchain Records Can and Cannot Do

Many SPV-based fractional platforms use blockchain to record profit rights certificates. A blockchain record is tamper-resistant, transparent, and time-stamped — it provides a strong audit trail. However, Furthermore, Section 65B of the Indian Evidence Act, 1872 treats blockchain records as electronic records. Courts require a Section 65B certificate for their admissibility in legal proceedings.

This limitation does not make blockchain records worthless. It means investors should treat a blockchain certificate as a transparency tool and supporting record — not as a standalone legal instrument.

As a result, the Trust deed and the registered property documents remain the primary legal evidence of rights. Importantly, platforms that present blockchain records as legally equivalent to registered title are overstating their value.

What to Check in an SPV Structure Before You Invest

Five Questions to Ask

Before committing capital to any SPV-based fractional investment, work through these five checks. First, ask who the Trustee is and whether they operate independently of the platform company. Second, request the Trust deed and confirm it names the beneficiaries, specifies the distribution policy, and documents the exit mechanism. Third, ask whether the property title chain is clean and independently verifiable. Fourth, confirm that the SPV is a separate legal entity — the platform’s operating company should not be the sole trustee with no succession plan. Fifth, understand what “profit rights” means in the specific Trust deed you are investing into — the details matter.

For a complete verification checklist covering all five areas in detail, see our platform verification checklist.

Frequently Asked Questions

What does SPV stand for in real estate?

SPV stands for Special Purpose Vehicle. In real estate, it refers to a separate legal entity — typically a Trust or LLP — that holds a specific property on behalf of investors, keeping that asset legally separated from the operating platform.

How does an SPV in real estate protect investors?

The SPV holds the property in a separate legal entity. As a result, If the platform company becomes insolvent, the platform’s creditors cannot automatically access the SPV’s assets. The Trust deed’s terms — which govern investor rights — continue to apply to those assets independently.

What is the difference between a Trust-based SPV and an LLP-based SPV?

For example, a Trust-based SPV operates under the Indian Trusts Act, 1882, with a named Trustee holding legal title on behalf of beneficiary investors. An LLP-based SPV gives investors a form of membership in the LLP that holds the property. The Trust model is more common in fractional real estate because it clearly separates legal title (Trustee) from economic rights (investors).

Do investors get registered title when they invest through an SPV?

No. Specifically, investors receive profit rights via a co-ownership certificate — economic participation in the Trust’s assets, not registered title to the property. The Trustee holds legal title. This distinction affects tax treatment, exit options, and legal recourse.

Is a Trust/SPV fractional model the same as a SEBI SM REIT?

No. In fact, these are structurally and regulatorily different frameworks. In contrast, SEBI’s SM REIT framework requires exchange listing, mandatory disclosures, and a ₹10L+ minimum investment. Trust/SPV fractional models operate under the Indian Trusts Act, 1882 and do not require SEBI registration. Both have legitimate uses — they serve different investor profiles.

Ready to invest through a properly structured Trust/SPV?

Landbitt uses a registered Trust/SPV structure under the Indian Trusts Act, 1882 with an independent Trustee. You receive profit rights via an SPV NFT certificate — not registered title, not company equity. PMLA-compliant KYC. Starting from 1 sq. ft. or ₹20,000.