")

TL;DR: The Indian Trusts Act, 1882 is the legal foundation behind Trust-based fractional real estate investment in India. Under this Act, a named Trustee holds immovable property on behalf of beneficiaries under a written Trust deed. As a result, investors in Trust-structured fractional platforms receive profit rights — economic participation in the Trust’s assets — not registered title. Understanding this Act is therefore essential for evaluating any fractional investment platform that uses a Trust or SPV structure.

The Indian Trusts Act, 1882 Explained: What It Means for Your Investment

The Indian Trusts Act, 1882 is one of the oldest and most foundational laws governing property management in India. For fractional real estate investors, understanding this Act is not optional — it determines the legal basis for every Trust-structured investment platform operating in India today.

The Indian Trusts Act, 1882 is the legal backbone of Landbitt’s investment structure.

Every Landbitt investment is structured through a registered Trust under this Act. An independent Trustee holds registered title to each property; you hold documented profit rights via an SPV NFT certificate — not title, not company equity. PMLA-compliant KYC. Starting from 1 sq. ft. or ₹20,000.

Quick Facts

- Full name: The Indian Trusts Act, 1882 (Act No. 2 of 1882)

- Governs: The creation, administration, and enforcement of private Trusts in India

- Relevant sections for investors: Sections 5, 6, 11, 13, and 55–67 (beneficiary rights)

- Key relevance to fractional real estate: Allows a Trustee to hold immovable property on behalf of multiple beneficiaries under a written Trust deed

- Limitation note: The Act covers private Trusts. Public Trusts and religious or charitable Trusts fall under separate legislation at the state level.

What Is the Indian Trusts Act, 1882?

The Core Purpose

The Indian Trusts Act, 1882 codifies the law of private Trusts in India. Parliament enacted it to bring clarity and legal enforceability to Trust arrangements — specifically, where one party (the Trustee) holds property for the benefit of another party (the beneficiary). Before this Act, Trust law in India relied primarily on English equity principles without a unified statutory framework.

For real estate investors, the central achievement of this Act is straightforward: it makes it legally possible for a Trustee to hold property on behalf of many beneficiaries simultaneously, with each beneficiary’s rights clearly defined in a written Trust deed. Consequently, this mechanism is what enables fractional real estate investment in India at scale.

Key Definitions Under the Act

Trustee, Beneficiary, and Trust Property

Section 3 of the Indian Trusts Act, 1882 defines a Trust as “an obligation annexed to the ownership of property, and arising out of a confidence reposed in and accepted by the owner, or declared and accepted by him, for the benefit of another, or of another and the owner.” In plain terms, someone holds property not for themselves but for someone else’s benefit.

In a fractional real estate Trust, three roles apply. First, the settlor creates the Trust and transfers property into it. Second, the Trustee accepts the legal obligation to hold and manage that property for the beneficiaries’ benefit. Third, the beneficiaries — the investors — are the parties for whose benefit the Trust exists. The Trust deed is the written document governing all of this: it names the Trustee, identifies the property, defines the beneficiaries’ rights, specifies the distribution policy, and sets out the exit mechanism.

How the Indian Trusts Act, 1882 Enables Fractional Real Estate

The Sections That Matter Most for Investors

Section 5 of the Act states that any kind of property — including immovable property such as land and buildings — can transfer into a Trust. This single provision makes it legally possible for a fractional real estate platform to hold a property inside a Trust and give multiple investors a documented interest in that property. Without Section 5, the Trust-based fractional model would have no statutory basis.

Trustee Duties and Beneficiary Rights

Moreover, Section 11 sets out the Trustee’s duty of care: the Trustee must act with the care of a person of ordinary prudence dealing with their own property. This duty therefore protects beneficiaries from negligent or self-interested management. In addition, Sections 55 to 67 govern beneficiary rights specifically: Section 55 gives beneficiaries the right to demand Trust performance, Section 63 gives them the right to inspect and copy Trust documents, and Section 67 allows them to sue the Trustee for breach of Trust.

What Investors Actually Hold: Profit Rights vs Registered Title

A Critical Legal Distinction

Investing through a Trust-based fractional platform does not give you registered title to the property. Instead, the Trustee holds legal title — their name appears in the government land records. You, as a beneficiary or profit rights holder, receive economic participation: a documented share of income and proceeds from the Trust’s assets.

Importantly, platforms may describe this position using different terms — some say “beneficial interest” and others say “profit rights.” Both refer to a documented economic entitlement to income and proceeds from the Trust’s assets rather than registered title. The words matter significantly — read the Trust deed carefully to understand exactly what your certificate entitles you to, and whether your rights are enforceable under the specific Trust structure the platform uses.

Furthermore, this distinction affects tax treatment, exit options, and legal recourse. Income from Trust distributions may attract different tax treatment than rental income from direct ownership. Exit depends on the Trust deed’s liquidity provisions, not open-market property sale. For a full breakdown of how the SPV structure uses this Act, see our guide to SPV in real estate explained.

The Trust Deed: What to Check Before You Invest

Five Clauses That Determine Your Protection

The Trust deed is the governing document of your investment. While the Indian Trusts Act, 1882 sets the legal minimum, the Trust deed determines the actual terms of your specific investment. Before committing capital, therefore, verify that these five clauses are present and clearly written.

First, check the beneficiary identification clause: does the deed name investors as beneficiaries or profit rights holders, and does it specify how new investors are added? Second, examine the distribution policy: how and when does the Trust distribute income and proceeds? Third, review the Trustee succession clause: what happens if the current Trustee resigns or is removed? Fourth, confirm the exit mechanism: can investors sell their certificates, and under what conditions? Fifth, verify the breach of Trust remedy: does the deed specify a clear process for raising complaints against the Trustee?

A well-drafted Trust deed under the Indian Trusts Act, 1882 covers all five clearly. For a complete verification checklist covering platform legal structure, see our platform verification checklist.

The Evidence Act Section 65B Limitation

Blockchain Records Are a Supplement, Not a Substitute

Many Trust-based fractional platforms record investor holdings on a blockchain. A blockchain record creates a tamper-resistant, time-stamped audit trail — a genuinely useful transparency tool. However, Section 65B of the Indian Evidence Act, 1872 requires a certificate for blockchain records to be admissible as electronic evidence in court proceedings.

As a result, the Trust deed and its registered version with the sub-registrar remain the primary legal instruments. A blockchain certificate supplements them — it does not replace them. Platforms that describe blockchain records as equivalent to registered title or as independently sufficient legal instruments are overstating the current position under Indian evidence law.

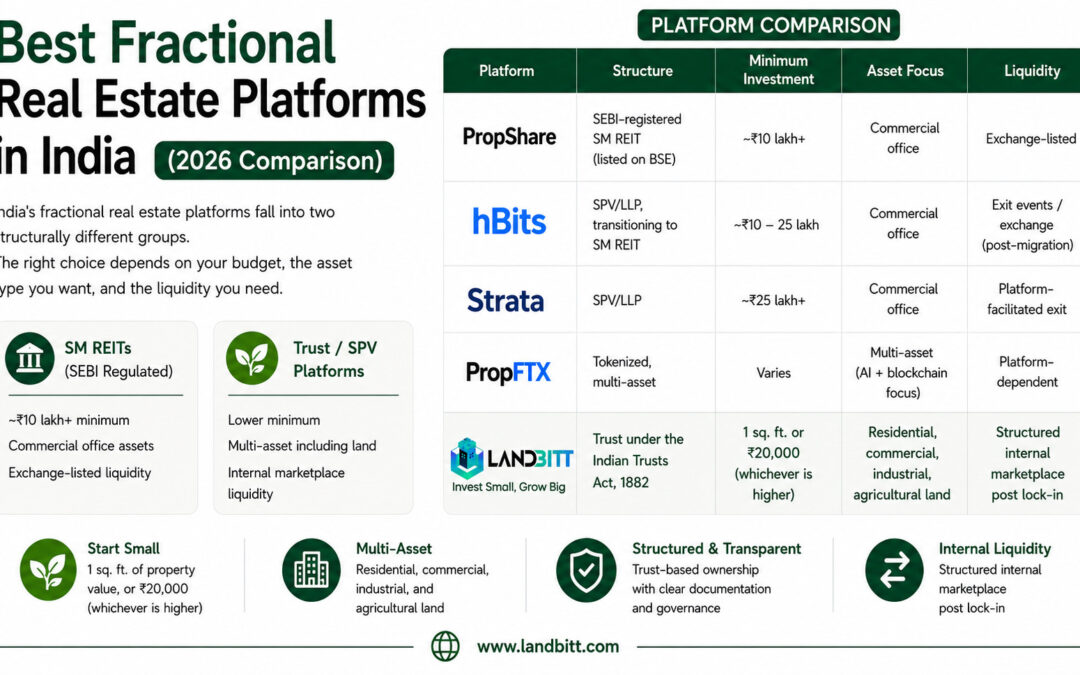

Indian Trusts Act, 1882 vs SEBI SM REIT Framework

Two Distinct Frameworks

SEBI introduced the SM REIT framework through amendments to its REIT Regulations in 2023. SM REITs are exchange-listed investment vehicles subject to SEBI oversight, mandatory disclosures, and a minimum investment of ₹10 lakh per unit scheme. Consequently, they represent a separate regulatory framework entirely from the Indian Trusts Act, 1882.

Trust-based fractional platforms do not operate under SEBI’s SM REIT framework. Instead, they operate under the Indian Trusts Act, 1882 and general contract law. They are not exchange-listed. As a result, these two frameworks serve different investor profiles and carry different regulatory protections — neither is categorically safer than the other without considering the specific implementation.

Frequently Asked Questions

What does the Indian Trusts Act, 1882 actually allow in real estate?

The Act allows a named Trustee to hold immovable property — land, buildings, or any real estate — on behalf of beneficiaries under a written Trust deed. Section 5 explicitly permits immovable property to transfer into a Trust. This is therefore the legal mechanism behind every Trust-based fractional real estate platform in India.

Do I get registered title when I invest through a Trust-based platform?

No. The Trustee holds registered title — their name appears in the government land records. You hold a documented interest in the Trust (either as a named beneficiary or as a profit rights holder via a certificate). This gives you economic participation rights, not direct ownership of the underlying property.

What rights do I have as a beneficiary under the Indian Trusts Act, 1882?

Sections 55–67 of the Act give beneficiaries the right to demand Trust performance, inspect Trust documents (Section 63), and sue the Trustee for breach of Trust (Section 67). In practice, however, your specific rights depend on the terms in the Trust deed — the Act sets the minimum floor, not the ceiling.

What happens if the Trustee acts against my interests?

Section 67 of the Indian Trusts Act, 1882 allows beneficiaries to bring a legal action against a Trustee for breach of Trust. You would need to demonstrate that the Trustee violated their duty of care (Section 11) or breached the specific terms of the Trust deed. The process runs through civil courts, not a regulatory body.

Is a Trust-based fractional platform the same as a SEBI-regulated SM REIT?

No — these are entirely different legal and regulatory frameworks. Trust-based fractional platforms operate under the Indian Trusts Act, 1882. SEBI SM REITs operate under SEBI’s REIT Regulations (as amended in 2023), are exchange-listed, and require a ₹10L+ minimum investment. They are therefore not interchangeable.

Invest with the legal clarity of the Indian Trusts Act, 1882 behind you.

Landbitt uses a registered Trust/SPV structure with an independent Trustee holding title to each asset. You hold profit rights via an SPV NFT certificate — not registered title, not company equity. PMLA-compliant KYC. Starting from 1 sq. ft. or ₹20,000.